TL;DR:

- Restaurant space valuation focuses solely on real estate factors, separate from business performance.

- Key metrics include sales per square foot, rent-to-sales ratio, and capitalization rates.

- Lease terms, tenant quality, and build-out costs significantly influence property value.

Most restaurant owners assume that valuing a space is simply part of valuing the business. It is not. Restaurant space valuation is a separate discipline focused purely on real estate factors, not on your sales volume, brand equity, or goodwill. This distinction matters enormously when you are deciding whether to buy, lease, or walk away from a location. Pay too much for the wrong space and no amount of great food will save your margins. Understand the real drivers of space value and you gain a genuine competitive edge before you sign anything.

Table of Contents

- What is restaurant space valuation?

- Core methods of restaurant space valuation

- Key benchmarks: Rents, sales, and cap rates

- Critical factors: Lease terms, property type, and special situations

- Why most buyers get restaurant space valuation wrong—and how to avoid it

- Find quality restaurant spaces with expert-backed valuation support

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Space vs business valuation | Restaurant space value focuses only on the real estate, not operational profits or goodwill. |

| Main valuation methods | Income, sales comparison, and cost approaches offer different views—use the right one for your scenario. |

| Benchmarks matter | Check sales per square foot, rent ratios, and cap rates to ensure your deal is in market range. |

| Lease terms change value | Lease length, rate, and tenant quality can swing value more than most buyers realize. |

| Expert support helps | Using trusted frameworks and listings makes it easier to secure a space that adds value to your restaurant business. |

What is restaurant space valuation?

Restaurant space valuation means appraising the real estate component of a food and beverage property. That is it. You are not measuring how profitable the restaurant inside is, how loyal the customers are, or how much the owner spent on the kitchen. You are measuring what the physical location is worth as a piece of commercial real estate, adapted for the specific risks and features of the food service industry.

Business valuation, by contrast, factors in everything: sales revenue, goodwill, brand value, and FF&E (furniture, fixtures, and equipment). The two are related but separate. A restaurant business might sell for $800,000 while the space it occupies is worth far more or far less on the real estate market, depending on lease terms, condition, and location demand.

Why does this distinction matter? Because buyers, tenants, and investors often make critical errors by blending the two. An operator who conflates strong sales with a strong property value can overpay for a location that carries hidden real estate risks.

Here are the restaurant-specific risks that make space valuation uniquely complex:

- High tenant turnover: Restaurants fail at higher rates than most retail businesses, which increases vacancy risk for landlords.

- Expensive build-outs: Custom kitchen infrastructure, grease traps, and ventilation systems cost hundreds of thousands of dollars and do not always add portable value.

- Lease and layout constraints: Below-market rents, unusual lease structures, or awkward floor plans can severely limit what a buyer is willing to pay.

- Permit dependencies: Health permits, liquor licenses, and zoning approvals are location-tied and can either add or subtract from value.

“Restaurant space valuation uses standard commercial real estate methods adapted for food and beverage properties, accounting for unique risks like high tenant turnover and specialized infrastructure.”

Getting this right starts with understanding restaurant real estate basics before you ever walk into a negotiation. If you have general questions about how these deals work, exploring restaurant space FAQs can clarify the process quickly.

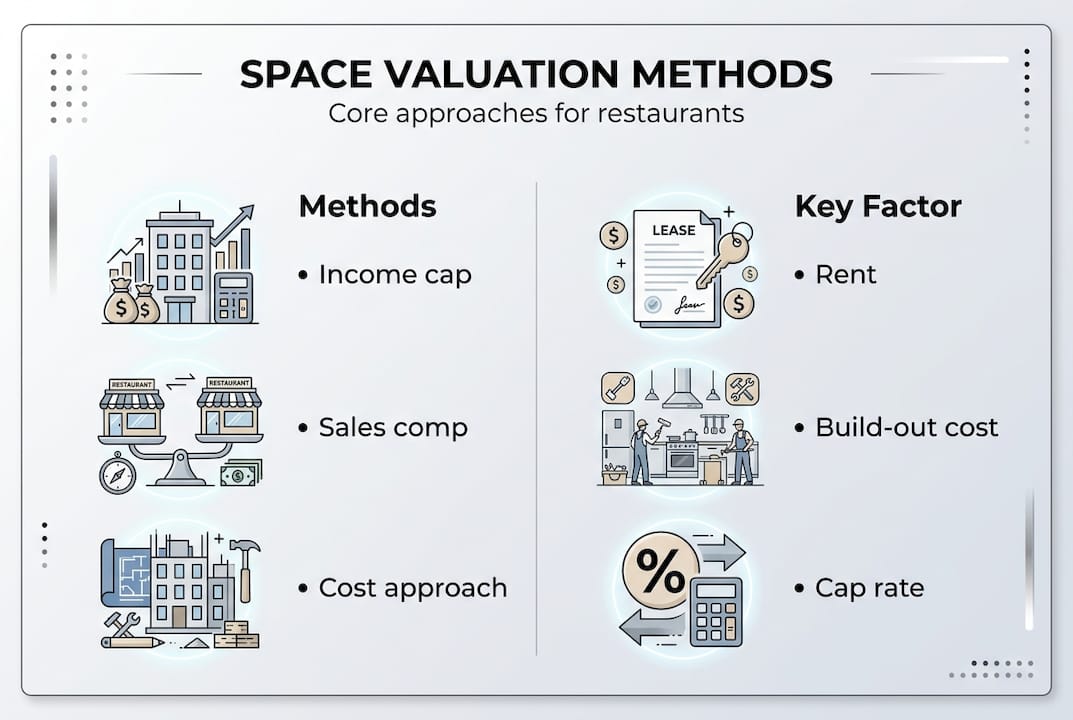

Core methods of restaurant space valuation

Appraisers and investors use three primary methods to determine what a restaurant space is worth. Each has strengths, weaknesses, and appropriate use cases. Most experienced buyers use a combination rather than relying on any single method.

-

Income capitalization approach: This method calculates value by dividing the property’s Net Operating Income (NOI, meaning rent income minus operating expenses) by the local market cap rate. For example, a property generating $120,000 in annual NOI at a 6% cap rate would be valued at $2,000,000. This method works best when the space is already leased and generating stable income.

-

Sales comparison approach: Here, appraisers look at recent sales of comparable restaurant spaces in the same market, adjusting for differences in size (price per square foot), lease terms, condition, and location. This method is most useful when there are enough nearby sales to build a reliable comparison set.

-

Cost approach: This calculates the land value plus what it would cost to rebuild the structure from scratch, then subtracts depreciation. It is less common for restaurant leases but matters when evaluating owner-occupied buildings or new construction.

| Method | Strengths | Best for |

|---|---|---|

| Income capitalization | Tied to actual cash flow | Leased investment properties |

| Sales comparison | Market-grounded, intuitive | Active sale markets |

| Cost approach | Good for new or unique buildings | Owner-occupied, new builds |

Three primary methodologies are recognized across commercial real estate, with income capitalization the most relied upon for income-producing restaurant spaces.

Pro Tip: For leased restaurant properties, the income approach is the most relevant. But for owner-operators who occupy their own building, use a hybrid of income and cost methods, since there is no market rent to anchor the income calculation. You can read more about this in our valuation methods guide.

Understanding restaurant build-out costs is also essential here, since expensive infrastructure can inflate the cost approach estimate while not always delivering equivalent market value.

Key benchmarks: Rents, sales, and cap rates

Once you understand the methods, you need reference points to judge whether a specific space is overpriced, attractively valued, or a risk worth taking. These benchmarks give you a practical lens.

Sales per square foot is one of the clearest indicators of how productive a space can realistically be. Full-service restaurants average $150 to $250 per square foot in annual sales, while counter-service and quick-service concepts typically land between $200 and $300 per square foot. If a landlord is pricing rent based on projections far above these ranges, that is a warning sign.

Rent as a percentage of gross sales is arguably the most critical ratio for operators evaluating space cost. Industry best practice is to keep rent below 7% of gross sales. Anything approaching 10% starts to stress operations. Above 10% is high risk territory for most concepts.

| Metric | Healthy range | Caution zone | High risk |

|---|---|---|---|

| Rent as % of sales | Below 7% | 7 to 10% | Above 10% |

| Full-service sales per SF | $150 to $250 | Below $150 | Below $100 |

| Counter-service sales per SF | $200 to $300 | Below $175 | Below $125 |

| QSR cap rate (2026) | 5.5 to 6.5% | Below 5% | Above 8% |

Cap rates reflect investor risk expectations. QSR cap rates average around 5.68% in competitive markets, with full-service properties typically carrying slightly higher rates due to greater operational risk. A lower cap rate means higher demand and a premium price. A higher cap rate means more risk or less desirable conditions.

For a deeper look at how these numbers connect to what investors actually pay, detailed valuation benchmarks from industry advisors provide additional context. You can also review lease term benchmarks to understand how rent structures interact with cap rate expectations.

Most sustainable operations keep rent below 7% of sales. If the math does not work at that threshold, the space is likely overpriced for your concept.

Critical factors: Lease terms, property type, and special situations

Numbers on a page only tell part of the story. Real-world variables can swing a restaurant space’s value dramatically up or down, even when the square footage and asking rent look comparable.

Lease length and tenant credit: A 10-plus year lease with a financially strong tenant is worth considerably more to an investor than a month-to-month arrangement. Stable, long-term leases reduce vacancy risk and allow investors to underwrite the property with confidence. Lease duration and tenant quality are among the most powerful value drivers in restaurant real estate.

Fee simple vs. leasehold ownership: Fee simple means the buyer owns the land and building outright. Leasehold means the building sits on land leased from a third party. Fee simple properties command significant premiums because the owner controls the full asset. Leasehold deals can still work, but the ground lease terms must be carefully reviewed since they cap the usable life of the investment.

Unique build-outs and tenant improvement costs: A custom sushi restaurant with imported stone counters and specialized ventilation may cost $500,000 to build but only $150,000 to replace with a flexible kitchen another operator can actually use. High specialty fit-outs often reduce rather than increase space value for buyers who need adaptability. More insight on how fit-out considerations factor into value is worth reviewing before assuming build-out dollars translate to appraised value.

Here is a checklist of factors that shift restaurant space value most significantly:

- Lease term remaining and renewal options

- Above-market or below-market rent relative to current conditions

- Escalation clauses (annual rent increases built into the lease)

- Tenant credit quality and personal guarantees

- Layout adaptability for different restaurant concepts

- Grease trap capacity, hood system, and ventilation specs

- Proximity to dense foot traffic or anchor tenants

- Commercial lease inclusions like CAM charges and exclusivity clauses

Pro Tip: Escalation clauses are the most commonly overlooked value factor. A lease with 4% annual rent increases looks manageable today but can price a tenant out of profitability within five years. Always model out the full rent stack over the lease term, not just the starting rate. Review restaurant lease types to understand which structures protect your position.

Why most buyers get restaurant space valuation wrong—and how to avoid it

The most common mistake we see is operators using business sale multiples to value just the space. Someone hears that a similar restaurant sold for 3x EBITDA (earnings before interest, taxes, depreciation, and amortization) and assumes that tells them something about the real estate. It does not. Business multiples and real estate cap rates measure fundamentally different things.

The second big miss is treating lease language as a formality. The difference between a favorable NNN lease (where the tenant pays taxes, insurance, and maintenance) and a gross lease (where the landlord covers those costs) can represent tens of thousands of dollars per year. That gap matters for both appraisal and operating reality.

Appraisers and business brokers also see value differently. Reconciling those perspectives requires anchoring to stabilized NOI using realistic, market-based lease terms, not the current operator’s sweetheart deal or inflated projections. Our view is that the smartest evaluators always request comparable lease abstracts (formal summaries of actual lease terms in the area) rather than relying solely on broker sales packages, which are built to sell, not inform.

For anyone starting this process, restaurant space selection tips can ground your search before you start comparing appraisal numbers.

Find quality restaurant spaces with expert-backed valuation support

Understanding how restaurant space valuation works is only useful if you can apply it to real properties with real numbers in front of you.

Pepperlot is built specifically for this moment. Every listing on the platform includes the restaurant-specific details that actually matter for valuation: seating capacity, grease trap specs, lease structure, and equipment included. You can see full restaurant listings from operators ready to lease, or browse available restaurant properties for sale with the infrastructure already in place. Whether you are underwriting your first space or your fifth, Pepperlot gives you the data and the listings to make a grounded decision.

Frequently asked questions

How is restaurant space value calculated differently from restaurant business value?

Restaurant space valuation focuses exclusively on real estate factors like rent, cap rate, and market comps, while business valuation includes sales performance, goodwill, and operational assets. The two should never be used interchangeably when making a leasing or purchasing decision.

What is a good rent-to-sales ratio for a restaurant?

The industry standard is to keep rent below 7% of gross sales, with rent above 10% of revenue considered financially risky for most restaurant concepts. Anything in between requires careful cash flow modeling before committing.

Which valuation method is best for owner-occupied restaurant spaces?

A hybrid of the income and cost approaches is most appropriate for owner-operators, since the absence of market-rate rent makes a pure income approach unreliable. Hybrid methods for owner-occupied spaces account for unique fit-out costs and real occupancy economics.

How do lease length and tenant credit affect value?

Long-term leases with financially strong tenants increase appraised value by reducing risk for investors, while short or weak leases lower it by introducing uncertainty about future income. This single factor can shift a property’s valuation by hundreds of thousands of dollars.

Recommended

- Restaurant Space with Business For Sale | PepperLot

- Restaurant Real Estate 101: How to Find, Lease, or Buy the Right Space for Your Concept | PepperLot Blog

- Second-Generation Restaurant Spaces: The Smartest Way to Launch Your Concept | PepperLot Blog

- Restaurant sale vs. lease: 4 key differences for success

- Waarom horeca kiest voor tapdrank: marge en efficiëntie

Leave a Reply